How to Build Wealth: Smart Investor’s Blueprint for 2025

Introduction

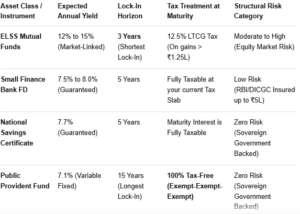

⚡ ELSS Funds: The Speed Demon of Tax Saving

For growth-focused investors, Equity Linked Savings Schemes (ELSS) represent the absolute gold standard of the Section 80C universe. It breaks the traditional mold of tax savers by introducing market-linked wealth creation to your tax planning.

The 3-Year Liquidity Edge

Every traditional 80C option requires you to part with your liquidity for a minimum of 5 to 15 years. ELSS completely disrupts this by offering a statutory lock-in period of just 3 years. This makes it the shortest lock-in tax saver available under Indian tax law. If you value financial agility, ELSS allows you to recycle your tax-saving capital far quicker than any insurance policy or government scheme.

High-Velocity Performance Realities

Unlike fixed-income options that struggle to outpace core inflation, ELSS funds invest directly in diversified equity portfolios. Over a long-term horizon, top-performing ELSS funds have historically delivered compound annual growth rates (CAGR) ranging between 12% and 15%. This compounding effect means your ₹1.5 lakh investment is actively building a substantial wealth corpus, rather than merely acting as a tax-shielding tool.

Navigating the Capital Gains Tax Structure

While the growth potential is unmatched, ELSS investments are not completely tax-free upon exit. Because they are equity assets, your returns are classified as Long-Term Capital Gains (LTCG). Under current tax provisions, LTCG on equity assets is taxed at a flat rate of 12.5% on gains that exceed the threshold of ₹1.25 lakh in a single financial year. Even with this tax applied, the net post-tax returns of ELSS consistently outshine traditional debt instruments.

🏦 Small Finance Banks: The Guaranteed 8% Fixed Income Play

Not everyone has the risk appetite for equity markets. If you prefer guaranteed, predictable returns but are tired of the meager 5.5% to 6.5% interest rates offered by major public sector banks, Small Finance Banks (SFBs) present a compelling alternative.

Capturing Aggressive Fixed Yields

To attract capital, several RBI-scheduled Small Finance Banks offer highly aggressive interest rates on their 5-year tax-saving fixed deposits. While traditional heavyweights lag behind, these nimble institutions regularly push tax-saver FD rates upwards of 7.5% to 8% for regular citizens, with an additional premium of 0.50% reserved exclusively for senior citizens.

The Safety Net: RBI-Backed Security

A common hesitation among conservative savers is the perceived risk of smaller banking institutions. However, Small Finance Banks are fully regulated by the Reserve Bank of India (RBI). Crucially, every depositor is completely protected under the Deposit Insurance and Credit Guarantee Corporation (DICGC) framework. This statutory insurance legally guarantees your principal and interest up to ₹5 lakh per bank, making a small finance bank tax saving FD just as safe as a traditional bank deposit within that limit.

Understanding the Tax Slab Drag

While the yield on these fixed deposits is highly attractive, you must keep an eye on the tax treatment of the interest earned. Unlike PPF, the interest accrued on a tax-saving FD is not tax-exempt. It is added directly to your annual income and taxed at your highest applicable marginal income tax slab. For individuals sitting comfortably in the upper tax brackets, this tax drag will reduce your net, post-tax yield.

⚖️ The Government Debt Showdown: PPF vs. NSC

If absolute sovereign safety is your non-negotiable benchmark, the choice inevitably narrows down to two legacy instruments managed by the Government of India: the Public Provident Fund (PPF) and the National Savings Certificate (NSC). However, matching these two head-to-head reveals stark differences in yield and liquidity velocity

The Yield Contrast

- National Savings Certificate (NSC): Offers a highly competitive, fixed interest rate of 7.7% compounded annually. The rate is locked in at the moment of purchase, protecting you from future interest rate cuts.

- Public Provident Fund (PPF): Currently provides a slightly lower interest rate of 7.1%. Unlike the NSC, the government reviews and resets the PPF interest rate every single quarter, exposing you to macro-economic rate fluctuations.

The Liquidity and Turnaround Clash

The Ultimate Tax Advantage: EEE vs. EET

📊 Head-to-Head 80C Instrument Comparison

🛠️ The Allocation Blueprint: Designing Your ₹1.5 Lakh Strategy

Maximizing your old regime benefits requires moving away from an “all-or-nothing” approach. Instead, map your ₹1.5 lakh Section 80C allocation directly to your life stage and risk tolerance using these three optimized allocation frameworks:

Framework 1: The High-Velocity Aggressive Asset Mix

- Target Audience: Young professionals, individuals under 35, or those with stable incomes and a high risk tolerance.

- The Strategy: Allocate 100% (₹1.5 Lakh) into ELSS Funds.

- The Outcome: This structure prioritizes compounding wealth above all else, ensuring your tax-saving money beats inflation while keeping your capital lock-in to the absolute minimum 3-year timeline.

Framework 2: The Balanced Wealth Builder Mix

- Target Audience: Mid-career professionals with family dependencies or investors seeking a balanced portfolio.

- The Strategy: Split your allocation evenly. Put 50% (₹75,000) into ELSS Funds for equity market growth, and 50% (₹75,000) into a High-Interest SFB Fixed Deposit or NSC.

- The Outcome: This balances risk perfectly. You capture market upside via equity while locking in a guaranteed, reliable income stream that returns to your bank account in 5 years.

Framework 3: The Ultra-Safe Capital Preserver Mix

- Target Audience: Risk-averse individuals, those approaching retirement, or investors with short-term capital preservation goals.

- The Strategy: Allocate 100% across NSC and PPF based on your long-term liquidity goals. Use NSC for a quick 5-year exit or PPF if you want a tax-free retirement nest egg.

- The Outcome: Your capital remains completely insulated from market volatility, backed by absolute sovereign safety, while maximizing your old regime tax deductions.

6. Stay Updated with Market Trends

Financial markets evolve. Keep learning to make informed decisions.

Ways to Stay Updated

- Follow financial news

- Read investment blogs

- Join investor communities

7. Plan for Retirement Early

Starting early ensures financial security. Take advantage of retirement plans like 401(k), IRAs, and pension funds.

Best Retirement Strategies

- Maximize employer contributions

- Invest in tax-saving retirement funds

- Diversify retirement portfolios

Conclusion

Wealth-building takes time and strategy. By setting goals, diversifying investments, leveraging technology, and minimizing debt, you can secure financial success in 2025 and beyond. Start today and stay consistent!

Disclaimer:

The information provided in this blog is for informational and educational purposes only and should not be construed as financial, investment, or legal advice. Equity investments are subject to market risks, and past performance is not indicative of future results.

This content does not constitute an offer, solicitation, or recommendation to buy or sell any securities, nor does it guarantee any specific financial outcome. Investors should conduct their own research, assess their risk tolerance, and consult with a certified financial advisor or investment professional before making any investment decisions.

The author and publisher of this blog are not liable for any financial losses, decisions, or actions taken based on the information provided. Invest wisely and at your own discretion.